Challenges of Stablecoins: Decentralization & Security

Explore the challenges of creating stablecoins that balance decentralization, security, and scalability. Analyze the failures of algorithmic stablecoins like Terra/UST, compare collateralized and a...

TECHNICALHISTORICALFUTURE SCOPE

1/27/20256 min read

Since the dawn of bitcoin in 2009, there has been market demand for stablecoins, that is by definition a cryptocurrency which holds equal value in relation to a nation’s fiat currency such as the US dollar or British pound or Australian dollar. This would allow it to be utilised with the same level of convenience and decentralisation as cryptocurrencies, while keeping its stable value in relation to the US dollar or other national currencies. Creating a stablecoin requires a balance the blockchain trilemma. These 3 critical elements are decentralisation, security and scalability which has proven to be a challenge for stablcoins time and time again. The top stablecoins within crypto remain highly centralised and lack resistance to government control which pose a challenge to create something better which can hold its peg against the US dollar, resisting a “death spiral” as seen in Do Kwon’s infamous UST “stablecoin” and many other failed algorithmic stablecoin attempts. The delicate balance of the blockchain trilemma will be explored and the possibilities for more censorship resistant functional stablecoins which will be crucial for the continued growth and maturity of the blockchain industry, enabling wider adoption and unlocking new possibilities for decentralized finance

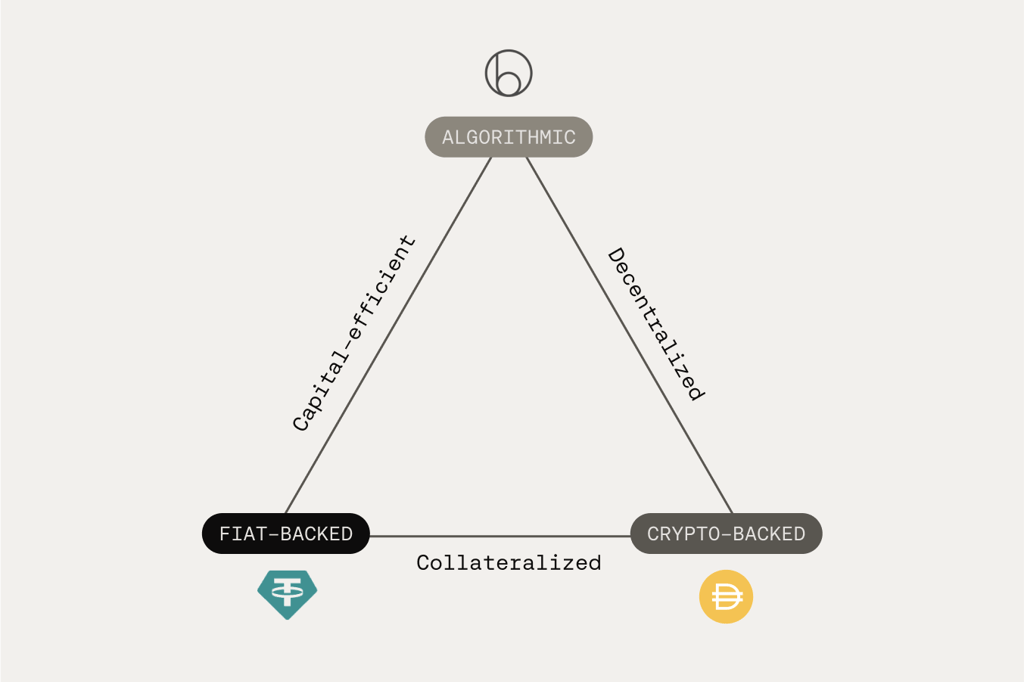

The types of stablecoins avaliable today include three main types, with each excelling in the two out of the three categories of the blockchain trilemma elements which are security, decentralisation and scalability. USDT is capital efficient (scalable) and secure as it relies on cash and cash equivalents stored within bank accounts managed by corporate entities. DAI is a crypto backed stablecoin which requires 150% deposit backing for ETH ($1.5 worth of ETH deposited to mint 1 DAI) and differing amounts of collateral depending on the type of cryptocurrency, making it much less capital efficient, and therefore not able to scale well, although decentralised and secure. Similarly there are commodity backed stablecoins such as PAXG, which is a gold backed stablecoin. This suffers from the same problem DAI does, due to the price of the underlying asset's fluctuating nature, a larger amount of collateral is required, making the stablecoin less capital efficient and therefore less scalable

The other main type of stablecoin which has been the achilles heel within the world of cryptocurrencies is the algorithmic type of stablecoin, which promises to solve the issues of capital efficiency with stablecoins which are either asset or commodity backed such as DAI and PAXG while addressing the issues of centralisation and censorship resistance as seen in stablecoins such as USDC and USDT, in essence the best of both worlds. A dream for the crypto space

An algorithmic stablecoin maintains its peg to the fiat currency determined by utilising market dynamics of supply and demand. This is done by creating opportunities for traders to make arbitrage profits by buying or selling the token in order to get it back to its predetermined price, which creates a strong market balancing force in theory

Algorithmic stablecoins are infamous for being problematic and becoming depegged, that is where the value of the coin does not maintain its value in relation to the national fiat currency it is attempting to emulate. There have been many attempts to create a successful algorithmic stablecoin dating all the way back to BitUSD back in 2014 of which none have had much long term success with the fall of UST wiping out 40 billion dollars and catalysing the crypto crash of 2022 due to its depegging, leading to panic selling, leading to more depegging which resulted in the stablecoin losing the vast majority of its value

Crypto has not shied away from attempting to create stablecoins. Here are some prominent examples of stablecoin launches over the last few years

Empty Set Dollar (ESD)

Dynamic Set Dollar (DSD)

Terra/UST (2022)

IRON/TITAN (2021)

Neutrino USD (USDN)

USDD (Tron's algorithmic stablecoin)

Frax (hybrid model combining algorithmic and collateral-backed)

DEI (Deus Finance) USDD

Magic Internet Money (MIM)

Ampleforth (AMPL) - though it's more of an elastic supply coin than a pure stablecoin

UST was created by Do Kwon, a South Korean tech entrepreneur, keen to address this market demand by creating a new type of algorithmic stablecoin. A blockchain was launched in April 2019 called Terra Luna, of which it had its own native token, ticker LUNA and stablecoin, UST. The idea was to create an incentive based system which would allow arbitrage opportunities when UST was either above $1 or below $1 in order to rebalance it back to its stable price at $1

If UST was above $1, traders would be able to burn $1 of LUNA and mint 1 UST, which would naturally bring the price of UST back down to $1 due to the selling of the asset and market forces driving it down until it hit $1, in which there is no more arbitrage opportunity for traders to profit.

If UST fell below $1, traders would be able to buy it and then burn it to mint $1 of LUNA, which would reduce the supply of UST, thus increasing the price back up to $1 due to market forces.

On first glance, this seems like a well made unique type of algorithmic system. A stablecoin in which all the shock and volatility is absorbed by a directly linked token within the ecosystemwhich has mechanisms in place to keep the stablecoin at $1 through minting and burning mechanisms. Unfortunately this proved to be a problematic system with crucial flaws such as the ominous sounding death spiral which lead to the collapse of the $40 billion dollar LUNA-UST system

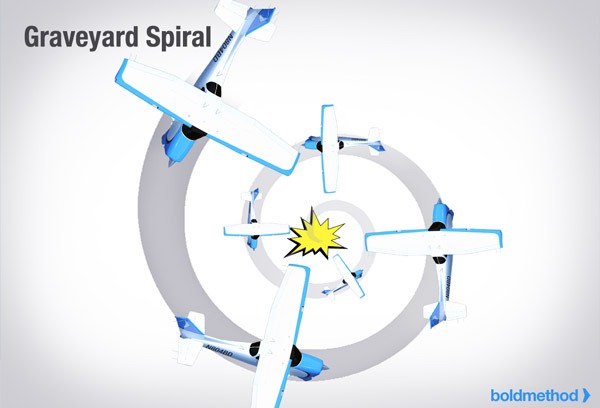

In aviation, a death spiral or graveyard spiral is where simply put, the unbalanced forces destabilises the aircraft due to poor handling during turning. The situation gets exceedingly worse with less and less and less hope of recovery as the death spiral becomes more and more intense leading to the aircraft spinning out into an unrecoverable position before crashing into the ground. The name given to what could potentially happen to UST during its operation was termed a death spiral by Vitalik before the demise of the system, not a pleasant flaw to be uncovered, but something that certainly should have been taken more seriously before the death spiral begun to take hold of the Terra Luna system

In more nuanced terms this occurred when too much selling of UST occurred, driving down the price. This created an arbitrage opportunity where the coin could be purchased and burnt to mint $1 of LUNA. Now as the price of UST remains below one dollar, more and more LUNA tokens are being minted, diluting the supply and reducing the price of the LUNA token. This leads to investors and token holders selling their accumulated tokens (bags), driving down the price of the token. This would mean that as each UST token is burnt and $1 of LUNA is created to attempt to rebalance the price of UST, more and more LUNA would be created as its price falls lower and lower, hence the name death spiral. To summarise:

Lower UST price → More LUNA minting

More LUNA minting → Lower LUNA price

Lower LUNA price → More LUNA needed per UST

And the cycle continues, accelerating the collapse as we see similarly in the case of our doomed aircraft

There have been many algorithmic stablecoins within the digital currency space, all with crucial flaws which prevent the token from being able to achieve the renowned trilemma being security, scalability and decentralisation. For now the market has decided that security and scalability are more important than decentralisation, as we live in a world with a high level of centralisation, so there is no big deal having a centralised token. But as time goes on, the market is more likely to move towards commodity and digital asset backed tokens as decentralization becomes a key part of the future. However unlikely, we may see an epic collapse of USDT or USDC, reiterating the key idea of cryptocurrencies and censorship resistance being a core tenant of the new decentralised era. Time will tell

Get in Touch

We'd love to hear from you! Reach out for questions, feedback or other enquiries

Reach

info@bitesizedblockchain.com

Bite Sized is not affiliated with these brands in any way

Grab your daily web 3 byte